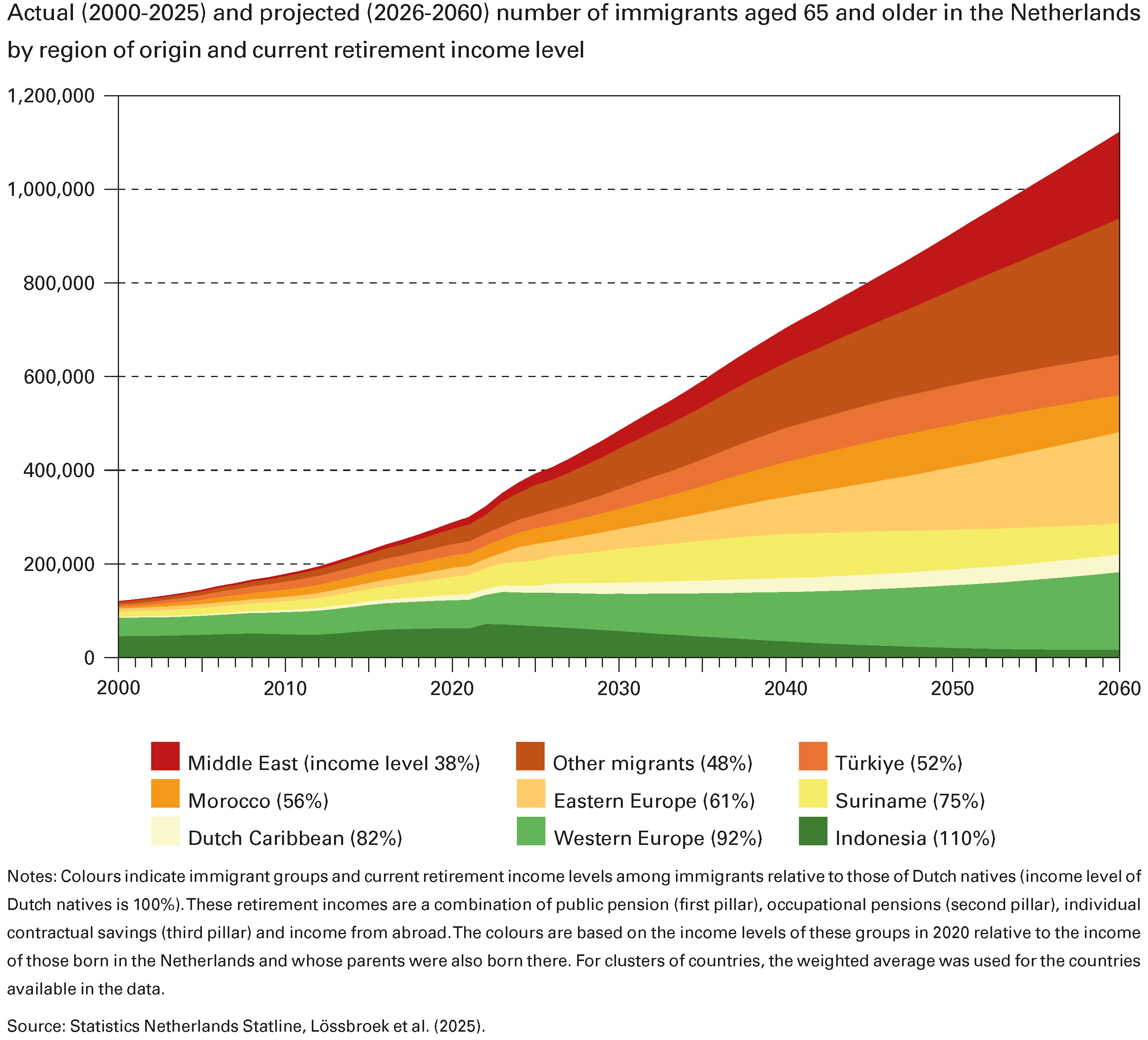

Across Western Europe, immigrants generally receive lower pension incomes than native-born citizens. In the Netherlands, immigrants from former colonies (Indonesia, Dutch Caribbean, Suriname) and Western Europe have on average higher retirement incomes than labour immigrants from Eastern Europe, Morocco or Türkiye, who in turn receive more than immigrants from other regions, particularly ‘refugee countries’. The figure below illustrates this pattern, showing immigrants’ retirement incomes relative to those of the native-born, ranking from comparable (green) to less than half (red). These retirement incomes combine public pensions (first pillar), occupational pensions (second pillar), individual saving provisions (third pillar) and pensions from abroad. Importantly, the fastest growth in numbers is expected among the groups with currently the lowest retirement incomes, whereas the number of the groups with comparable incomes, Indonesian and Western European immigrants, remains relatively stable. This means that the share of potentially vulnerable groups of immigrants increases.

What explains this ‘immigrant pension gap’? First, institutional policies determine access to public pensions, a main income source for many retirees. Given immigrants’ irregular work trajectories, public pension systems based on residence (like in the Netherlands) are more favourable than systems based on years worked or pre-retirement income. Compared to other residence- based systems, the pension income in the Netherlands is comparatively high, but it requires an exceptionally high 50 years of residence for a full public pension. Among immigrants, refugees often arrive at older ages and thus receive the lowest public pensions.

Second, socioeconomic factors often result in lower occupational pensions for immigrants: their shorter contribution period is exacerbated by labour market obstacles such as language barriers, a lack of educational credentials, discrimination, and concentration in sectors with weaker pension coverage. These vulnerabilities also limit opportunities to save privately for retirement. Western European immigrants can often partially compensate lower public and occupational pensions with retirement income from their country of origin, but this is uncommon among other immigrant groups.

Third, sociocultural factors affect immigrants’ private retirement savings. Many immigrants send remittances to family abroad, which reduces their savings capacity. Additionally, immigrants are often less aware of their accumulated pension income rights and options to improve them, and corrective action is therefore lacking. Lower levels of trust in financial institutions and traditions of informal saving further reduce voluntary participation in pension institutions. Retirees living below the social minimum could in many countries apply for means-tested welfare benefits, yet non-use of these facilities is a persistent issue, especially among immigrants, due to sociocultural factors. On the other hand, sociocultural factors can also form an informal safety net, as many retired immigrants receive financial and non-financial help from their family and social network.

Jelle Lössbroek, NIDI-KNAW / University of Groningen, e-mail: lossbroek@nidi.nl

Koen Veldman, NIDI-KNAW / University of Groningen, e-mail: veldman@nidi.nl

References

- Lössbroek, J., S. de Regt, M. Das, and T. Fokkema (2025), The retirement income of migrants in the Netherlands. Netspar Industry Paper 2025-21, Netspar, Tilburg.